There is a distinct, spine-chilling sensation that hits every Indian working professional around the 25th of the month. You open your banking app to make a quick UPI payment for a ₹20 cutting chai, glance at your remaining balance, and wonder if your bank account has fallen victim to an elaborate international heist. But deep down, you know there is no hacker—just your own weekend Swiggy orders and impulsive Amazon purchases staring back at you.

Saving money in India amidst 2026 inflation feels like trying to run up a down escalator. But you don't need a six-figure tech salary to build a solid financial cushion. With a simple, grounded framework, saving ₹1 lakh this year is entirely achievable without sacrificing your entire social life.

Why Most Savings Advice Does Not Work for Indians

If you search online for budgeting tips, you are immediately bombarded with generic Western advice like "cancel your daily Starbucks latte" or "invest in index funds." This advice completely misses the unique cultural reality of the Indian working professional. We aren't going broke buying $7 lattes; we are trying to balance family obligations, festive gifting, wedding expenses, and the rising cost of urban living on a normal Indian salary.

Furthermore, traditional Indian savings advice from our parents usually involves locking up every single rupee in a fixed deposit or buying physical gold. While well-intentioned, this rigid approach leaves zero breathing room for modern lifestyle expenses. To successfully save in 2026, you need a system that acknowledges your real life—one that accommodates occasional weekend outings while ruthlessly eliminating hidden financial leaks.

The Simple ₹1 Lakh Framework

When you set a massive goal like saving ₹1 lakh, it feels overwhelming and impossible. The secret is breaking it down into bite-sized, non-intimidating monthly milestones. To reach ₹1 lakh in twelve months, you need to save exactly ₹8,333 per month. That breaks down to roughly ₹274 a day—the exact cost of a gourmet burger or a premium auto ride during peak rush hour.

Once you view ₹8,333 as a non-negotiable monthly subscription to your future self, the math becomes incredibly straightforward. You don't need to live like a monk or stop meeting your friends. You simply need to identify the small, everyday habits where your money evaporates without giving you any genuine joy in return.

For instance, auditing your daily Swiggy and Zomato ordering habits, trimming redundant OTT family plans, and avoiding unnecessary mobile data top-ups can easily free up ₹3,000 to ₹4,000 a month. Add in a conscious effort to avoid surge-pricing cabs by taking the metro twice a week, and you have already hit half your target without feeling pinched.

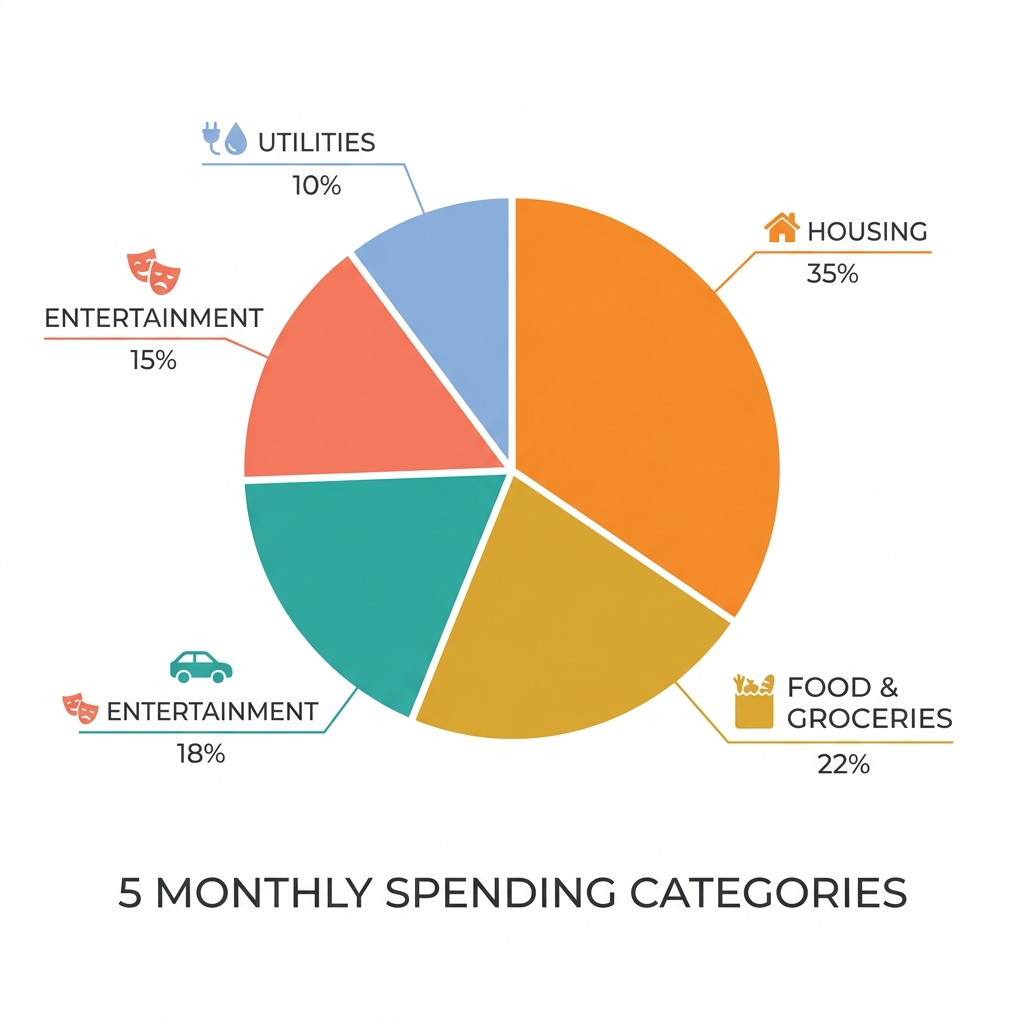

5 Categories Where Indians Overspend Without Knowing

To find that ₹8,333 every month, you need to know exactly where to look. Here are the five biggest culprits draining the modern Indian wallet.

1. Food Delivery (Swiggy & Zomato)

We often order food not because we are hungry, but because we are bored or tired after a long workday. A typical working professional easily spends ₹4,000 a month on delivery fees, packing charges, and overpriced restaurant items. Cutting this back to just two weekend orders saves you roughly ₹2,500 a month—amounting to ₹30,000 saved per year.

2. OTT & App Subscriptions

Between Netflix, Hotstar, Amazon Prime, SonyLIV, and premium music apps, you are likely paying for platforms you haven't opened in weeks. Consolidating these subscriptions or sharing family plans legally can instantly trim your monthly outgo by ₹800, saving you nearly ₹9,600 annually.

3. EMIs on Depreciating Items

No-cost EMIs feel like free money right up until your monthly salary gets swallowed entirely by smartphone and gadget payments. Avoid taking on debt for items that lose half their value the moment you open the box. Deferring that new phone upgrade saves you at least ₹3,000 a month in cash flow, totaling ₹36,000 a year.

4. Impulse Purchases on Sales

Every weekend brings a new "Mega Blockbuster Sale" across e-commerce apps designed to trigger FOMO. Buying a ₹3,000 jacket just because it was on a 50% discount doesn't save you ₹3,000—it costs you ₹3,000. Implementing a strict 48-hour waiting rule before checking out saves the average person around ₹1,500 monthly, or ₹18,000 a year.

5. Petrol & Ride-Share Services

Relying exclusively on Ola and Uber during peak surge hours or burning petrol in traffic jams takes a massive toll on your bank account. Switching to the metro or carpooling with office colleagues just three days a week easily saves ₹1,500 every month, putting an extra ₹18,000 back into your annual savings pool.

Best Free Tools to Track Your Spending in India

You cannot optimize what you do not measure. Tracking your spending manually on a notepad is exhausting, but thankfully, several excellent free apps automate the process perfectly for Indian banking systems.

Apps like Walnut (Axio) and Money View securely parse your bank SMS alerts to categorize your daily UPI expenses without requiring your net banking passwords. If you live with flatmates or split expenses with friends, Splitwise remains the absolute gold standard for ensuring you aren't silently overpaying for group dinners. Additionally, the built-in Google Pay spending tracker offers a fantastic visual breakdown of where your cash flows each month.

Pick exactly one tracking app today, allow it to monitor your transactions for thirty days, and prepare to be astonished by your actual spending patterns.

How to Automate Your Savings So You Never Forget

The single biggest mistake working professionals make is waiting until the end of the month to save whatever money is left over. In reality, there is never any money left over. The only foolproof way to save ₹1 lakh is to pay yourself first by automating your deductions.

Set up an automated monthly SIP (Systematic Investment Plan) or a Recurring Deposit (RD) with your bank that triggers exactly two days after your salary gets credited. By removing human discipline from the equation, your ₹8,333 gets safely tucked away before you even have a chance to look at it. Once the money is out of sight, you will naturally adjust your lifestyle to fit the remaining balance.

The goal here is not financial perfection; it is steady, automated consistency. For more money-saving guides made for India, bookmark incalw.me.

Frequently Asked Questions

Is ₹1 lakh savings realistic on a ₹30,000 salary?

Yes, though it requires intentional budgeting. Saving ₹8,333 represents roughly 27% of a ₹30,000 salary, leaving you with ₹21,667 for rent, groceries, and living expenses—which is highly manageable if you minimize dining out and avoid expensive EMIs.

Which Indian app is best for budget tracking?

Axio (formerly Walnut) is widely considered the best automated budget tracker in India because it seamlessly categorizes your UPI payments and credit card transactions via SMS without accessing your bank accounts.

Should I save first or invest first?

Always build an emergency cash fund in a high-yield savings account or liquid mutual fund first. Once you have accumulated three to six months of basic living expenses, you can confidently redirect your monthly savings into equity SIPs for long-term growth.